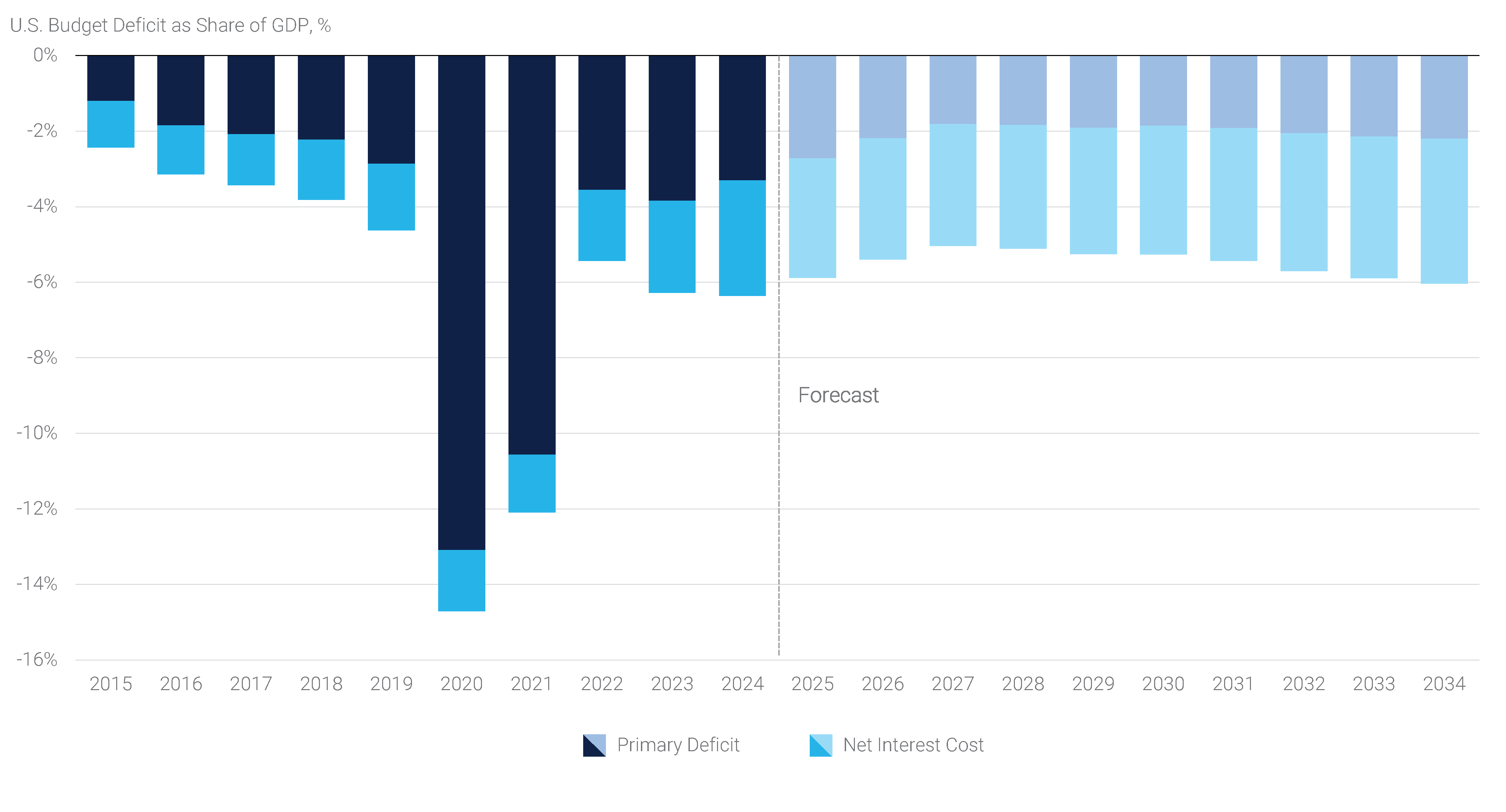

Primary Deficits Expected to Remain Meaningful

Global sovereign yield curves reinforced the shift higher in Treasury yields, with a notable selloff in Japanese Government Bonds (“JGBs”). Long-end Japanese yields climbed to record highs following weak bond auctions at the end of the month, continuing a trend that’s been building for some time, with the 40-year JGB yield rising nearly 100 bps since early April. These moves are occurring as Japan’s central bank gradually steps away from ultra-accommodative monetary policy, leaving long-end yields more exposed to market dynamics and creating a more price-sensitive demand picture.

Agency MBS

Agency MBS delivered modestly positive returns in May, benefiting from lower implied rate volatility and the broader move higher in yields. As interest rates rose, investors gravitated toward higher coupon securities to capture more attractive carry and reduce exposure to prepayment risk in a higher rate environment. Real money demand returned after a slower April, helping to stabilize the sector. The Bloomberg U.S. MBS Index recorded 19 bps of excess return over the month.

Additionally, headlines around GSE reform re-emerged, with signs that the Trump-era push toward privatization has gained momentum following two social media posts from the President late in May. While market participants broadly acknowledge the complexity of removing the GSEs from federal conservatorship, the increased focus raised uncertainty and potential for structural changes in the mortgage market. Despite these headlines, policymakers appear aware of the need for a gradual, well-communicated process that avoids major disruptions to mortgage credit availability and rates.

Equities, Credit, and Currencies

In contrast to the rate selloff, equities ended the month with gains as the S&P 500 delivered a 6.3% total return – the strongest May in at least two decades. Investors appeared to take comfort in continued economic resilience, solid corporate earnings, and extended tariff relief. While valuations remain stretched in some sectors, the market largely shrugged off higher yields as growth expectations remained intact.

Credit markets also performed well, with both investment grade and high yield spreads tightening. Healthy demand, stable fundamentals, and supportive technicals drove strong performance across the board. Corporate spreads tightened to levels seen in March, helping the Bloomberg U.S. Aggregate Corporate Bond Index post 127 bps of excess return for the month.

The Dollar, despite the rise in U.S. yields, finished the month slightly lower. This reflects, in part, the global nature of the bond selloff — rising yields abroad helped offset the relative rate advantage typically enjoyed by the Dollar. Additionally, ongoing uncertainty around U.S. fiscal policy and tariffs also weighed on sentiment. While the economic backdrop has improved, investors remain cautious given elevated deficits and the fact that average U.S. tariff rates are still well above pre-2025 levels.

Slowing Housing Demand Pressures Inventories

After the Fed began hiking interest rates in 2022, many market observers expected weakness in the housing market and a softening in home prices, as housing affordability deteriorated meaningfully. Home prices ultimately remained relatively firm, rising 6.9% and 4.8% in 2023 and 2024,(2) respectively, as low inventories offset slowing demand from potential home buyers. Fast forwarding to today, affordability remains challenged given high mortgage rates and high housing costs. However, inventories have grown, in large part driven by continued lackluster housing demand, resulting in a slowing of home price appreciation.

Elevated mortgage rates remain the biggest impediment to affordability, as the 30-year fixed rate mortgage measured by Freddie Mac averaged 6.8% in May, above levels seen last September, before the Fed cut interest rates by 100 bps. The higher rates are caused by elevated long-end Treasury yields and wide mortgage spreads. Home price levels remain well above pre-pandemic levels, rising 57% from the 2019 year-end levels, while median family incomes are only 29% higher over the same period. The combination of rising prices and high mortgage rates have kept annual mortgage payments as a share of family income near a historically elevated 25% for three consecutive years (see panel 3). To make matters even more challenging for potential home buyers, this share does not account for rising property taxes and insurance premiums.

Panel 3:

Housing Affordability Remains a Challenge

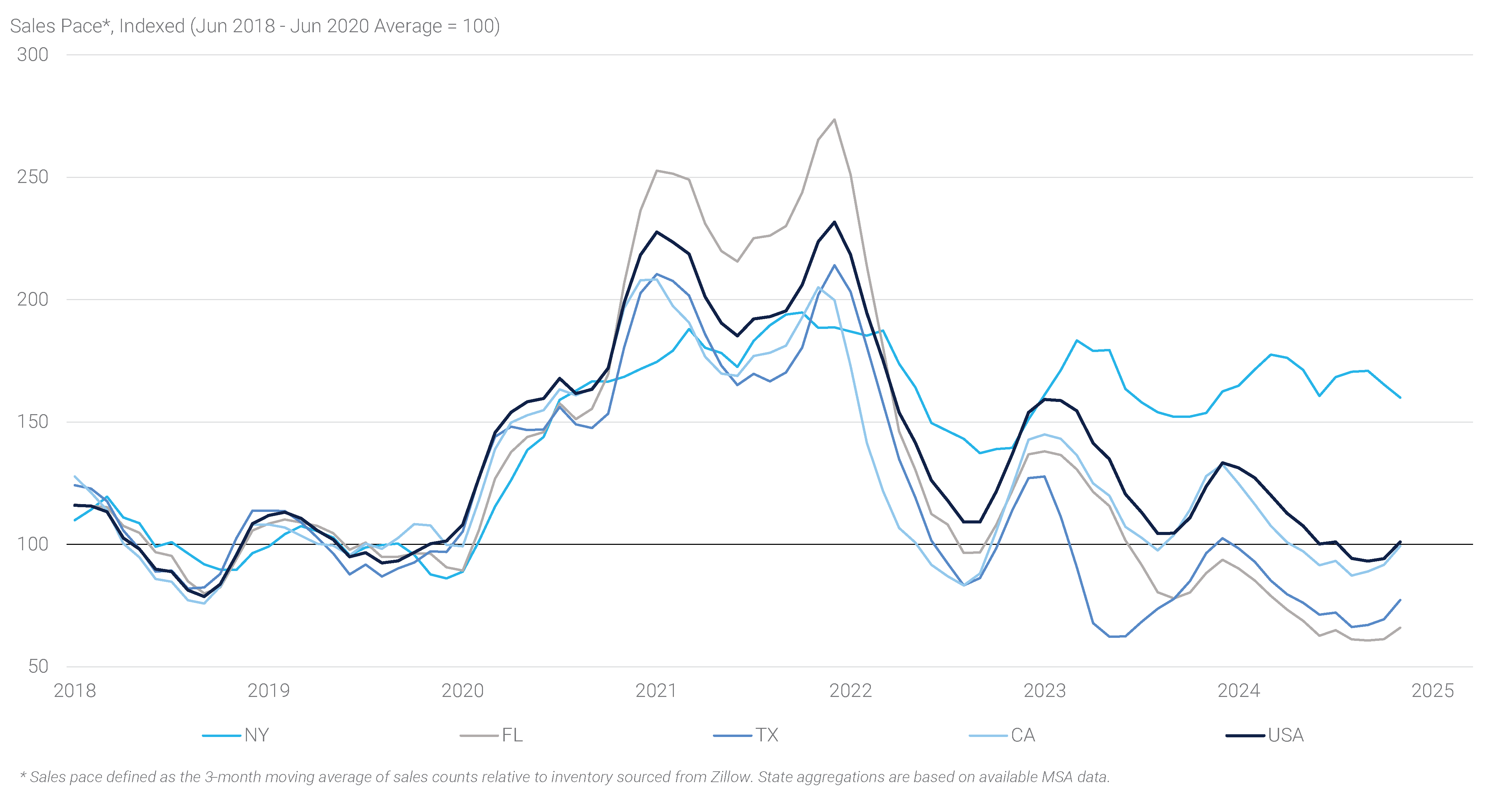

The rise in inventories appears to be driven by a continued slow pace of sales, rather than a flood of listings, implying homeowners are forced or are economically incentivized to move. Using Zillow data, we calculate the sales pace for several large states (see panel 4). As shown, this pace has normalized across the country but slowed more meaningfully in Florida and Texas, two states that benefited from migration in the aftermath of the pandemic. Meanwhile, New York continues to see a sales pace well above average, helping to explain the lower inventory and stronger price gains.

Panel 4:

The Pandemic Housing Boom Is So Over

The combination of slow sales and poor affordability suggests that home price growth could continue to slow in coming months as inventories build. Notably, Zillow data for April already showed a second consecutive month-over-month decline in prices, indicating that official home price indices might show similar weakness when released towards the end of June. However, we expect the declines to be gradual as supply only marginally outpaces demand. Builders will continue to manage their pipelines as necessary, while few existing homeowners appear forced to list their inventory for sale. The housing market should therefore continue its hibernation at low levels of activity until affordability improves significantly or overwhelming supply drives prices much lower.