Economic data received in June continue to point to a robust economic growth backdrop. Consumer spending appears to have reaccelerated in Q2 after downward revisions in Q1, business investment is strong, and the labor market has shown improved hiring. At the same time, inflation has been the dominant macro concern with higher energy prices pressuring a broader set of price categories, in turn keeping the Fed focused on upside inflation risks.

Economic Growth and Inflation

The Bureau of Economic Analysis’ third estimate of Q1 GDP revised annualized growth to a 2.1% seasonally adjusted annualized growth rate (“SAAR”), essentially the same as the initial estimate, but somewhat higher than a subsequent revision. In the latest estimate, GDP growth was mechanically boosted by a smaller net trade drag from lower imports, but consumer spending was revised down to a modest 0.5% SAAR from 1.4% prior. The consumption downgrade was entirely driven by much lower services spending. As a result, real final sales to private domestic purchasers — a cleaner measure of underlying domestic demand — dropped to 1.7% from 2.4% SAAR.

However, the underlying spending weakness seen in Q1 appears to have improved in Q2. The May Personal Consumption Expenditures (PCE) report was generally better than expected, despite continued indications of a stretched consumer. Nominal personal consumption expenditures rose 0.7% in May and real spending advanced 0.3% month-over-month (“mom”). Consumption gains were broad-based with nominal services spending rising 0.6% mom and goods spending jumping 0.9% mom. The latter was primarily driven by new and used cars. Personal income also surprised to the upside, increasing 0.7% mom. That said, the details were less positive than the headline implied. The May increase mostly reflected increases in farm proprietors’ income driven by payments from the American Relief Act of 2025. Consequently, the data reinforced a theme that has emerged repeatedly throughout 2026: growth remains positive, but the composition increasingly relies on investment related to the AI buildout rather than household demand.

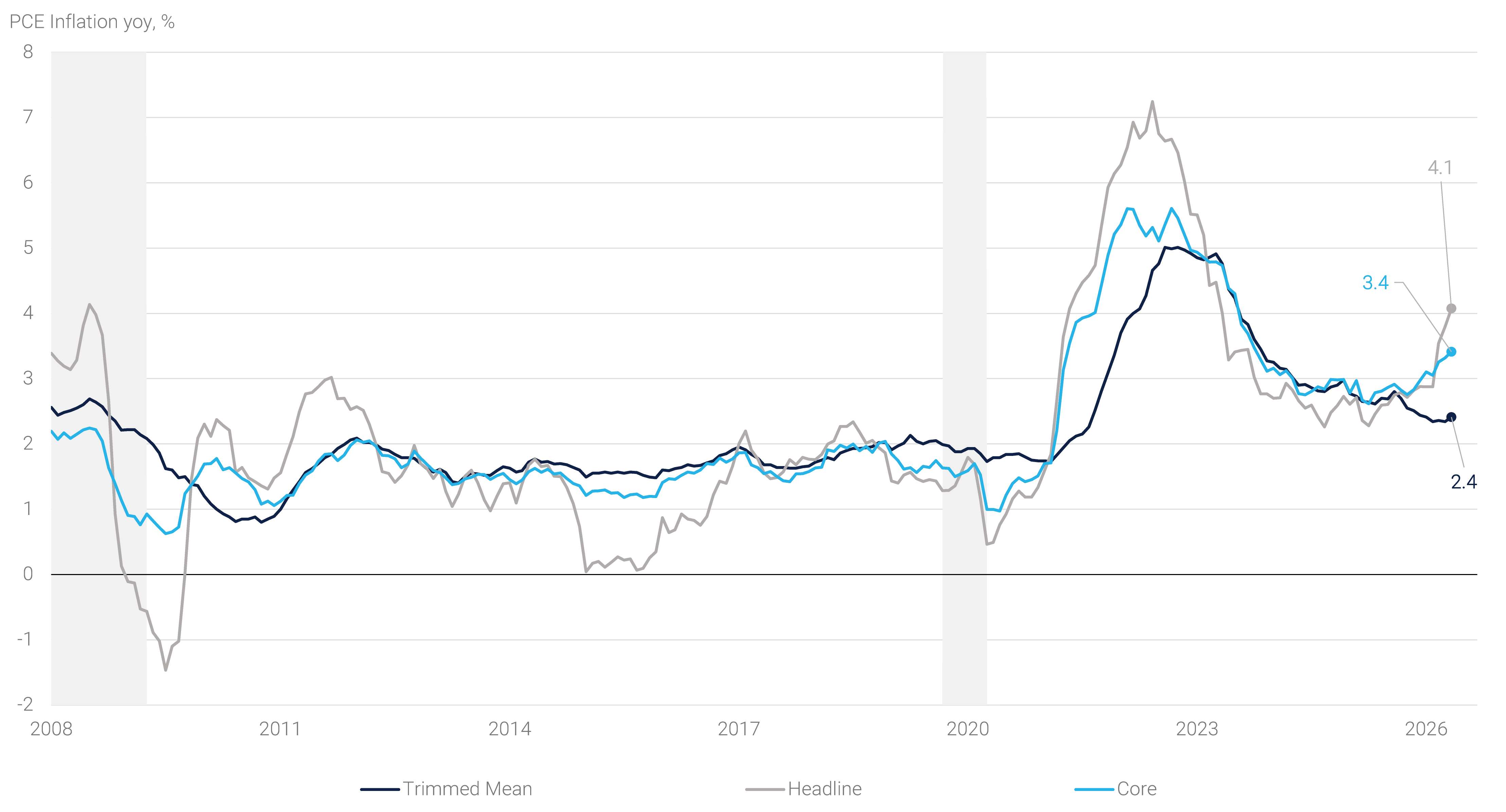

Turning to prices, as was broadly expected, the May PCE report delivered another reminder that inflation remains the primary challenge facing consumers, businesses, central bankers, and – with the midterm elections firmly in sight – politicians. Headline PCE prices increased 0.4% mom and 4.1% year-over-year (“yoy”), while core PCE rose 0.3% mom and 3.4% yoy. The annual core reading is now at the highest level since late 2023 and the gradual acceleration over recent months continues. Importantly, the inflation reacceleration no longer appears confined solely to energy prices. While these remain a major contributor, broader services inflation remains firm. On the positive side, the consumer and producer price indices reports suggested that the second-round effects from the surge in energy prices are slowing and that the tariff passthrough has largely come to an end, which should help keep services and commodity prices anchored. For the time being, however, pricing pressures remain inconsistent with a return to the Fed's 2% target notwithstanding alternative measures like the Dallas Fed trimmed mean PCE(1) having seen less pressure than the standard indices (see panel 1).

Panel 1:

PCE Inflation Remains Above Target

Labor Market

Turning to the labor market, the U.S. economy added 57,000 jobs in June according to the Bureau of Labor Statistics, a significant downtick from the number of jobs added last month and the trailing 3-month average pace of job growth. That said, the labor market remains healthy, with the 3-month moving average jobs created (111,000) still above most estimates of breakeven job growth. Meanwhile the unemployment rate declined to 4.2% with drops in employment being more than offset by a decrease in the labor force according to the household survey. Average hourly earnings rose 0.3% mom, in line with recent months, indicating that wage gains do not appear to be a major renewed source of inflation pressure.

Financial Markets

In addition to economic data, financial markets were driven by three major themes in June: a) the potential resolution of the conflict in the Middle East following the signing of the Memorandum of Understanding (“MOU”); b) the transition in Fed Chair; and c) the ever accelerating and capital-intensive AI buildout. Aspects from all three themes were seen across fixed income, equity, currency, and commodity markets.

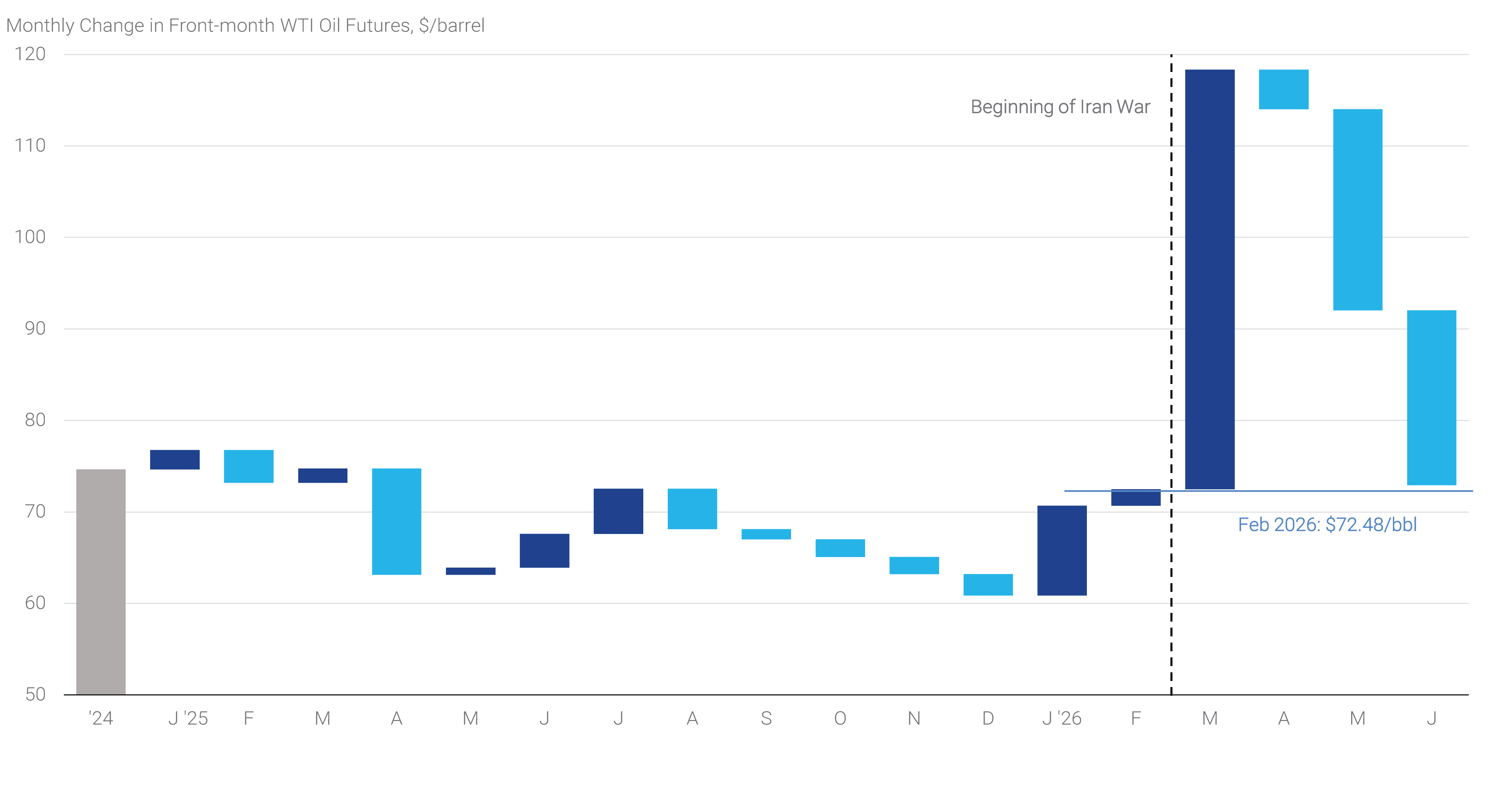

WTI crude oil futures prices declined over the course of the month, with oil prices falling back to levels seen in the early part of March, effectively reversing much of the war price premium seen in recent months (see panel 2). Of note, traffic in the Strait of Hormuz has increased since the MOU signing but remains well below pre-war levels. Oil markets nonetheless appear to have absorbed the meaningful supply shock much better than most strategists had expected.

Panel 2:

Oil Prices Have Reversed Virtually All of the War Premium

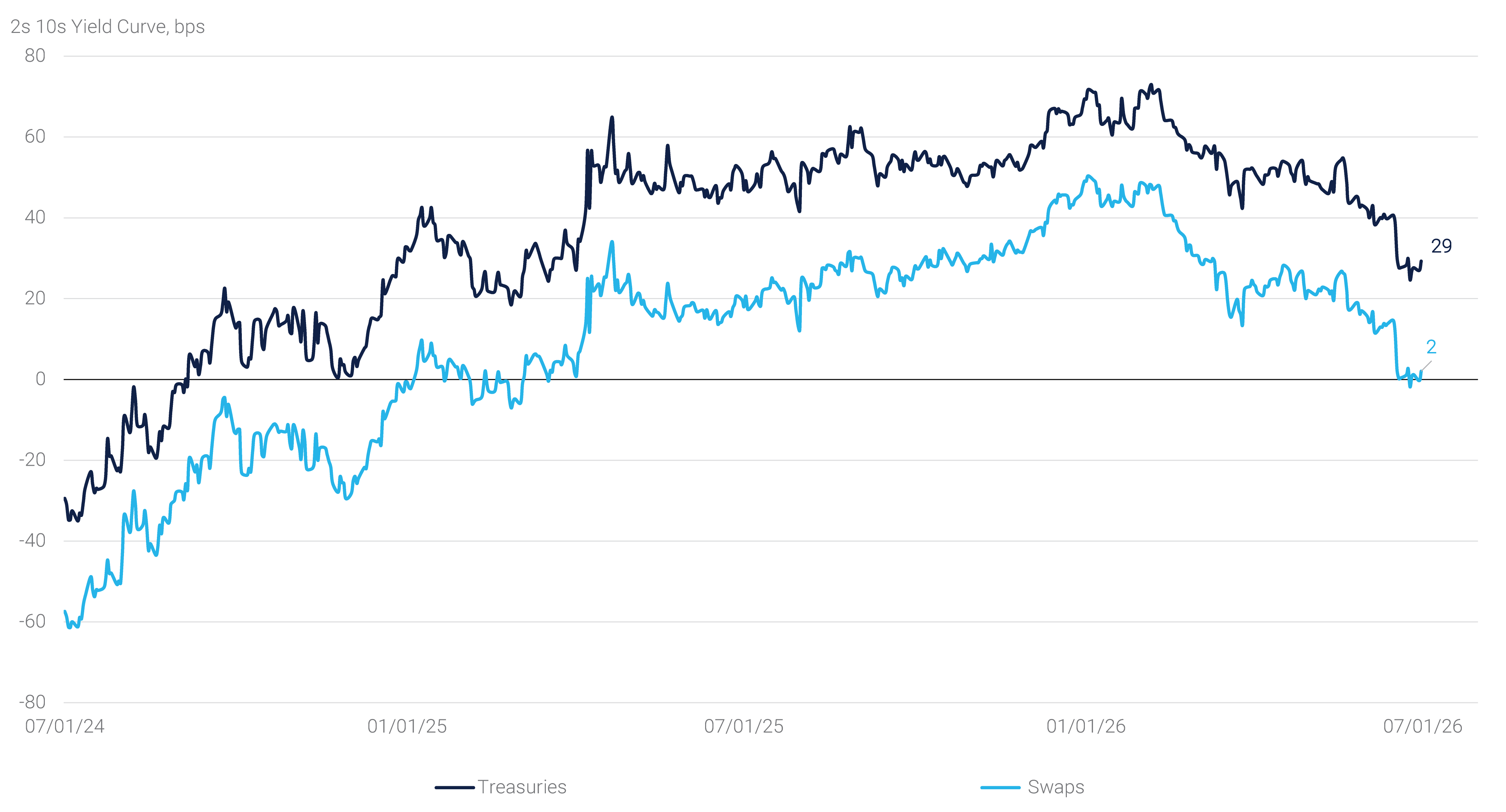

Despite the easing in oil prices, the Treasury yield curve continued its flattening, with 30-year yields ending June two basis points lower, at 4.95%, well below their 5.20% intraday peak back on May 20th. Shorter-term yields, meanwhile, rose as the economic narrative of firm inflation, solid economic activity, and a rebounding labor market increased the likelihood that the Fed could hike interest rates later this year (see panel 3). Pricing in overnight index swaps suggests market participants are expecting roughly 35 bps of hikes – the equivalent of one full hike and a one-third chance of a second – by the December FOMC meeting as of June 30th, well above the 15-bps priced at the end of May. The selloff in the front-end continued to drive flattening of the yield curve, with 2s-10s Treasuries ending the month at 29 bps, the flattest since April 2025. Of note, the 2s10s swap curve briefly touched inverted levels during June but ends the month modestly upward sloping.

Panel 3:

The Yield Curve Has Somewhat Reversed Its Steepening Trend

Meanwhile, interest rate markets showed muted price action in swap spreads in June, with 10-year swap spreads trading in a range of -40 to -42 bps during the month, one of the lowest realized ranges over the year. Interest volatility declined across tenors, with realized volatility showing a more meaningful decline than implied volatility over the course of the month.

Of note, the reform efforts by new Fed Chair Kevin Warsh (discussed below) and the hawkish messaging out the central bank have helped rebut the narrative about the “debasement trade” in recent months. Following several months of yield curve steepening and notable gains in gold, silver, and cryptocurrencies, those assets had poor returns in June specifically and 2026 more broadly, suggesting that markets have a newfound appreciation for the U.S. dollar and are less concerned about long-term inflation. The US Dollar Index ended June at the highest levels since the 2025 April tariff announcement, while the Japanese Yen fell to 40-year lows against the U.S. currency. In line with currency markets, Treasury price action was driven by real rates, reflecting the expectations for higher monetary policy rates and a robust economy, while inflation breakevens declined to some of the lowest levels over the past year. Following the apparent resolution of the Middle East energy price shock, markets show little concern about elevated longer-term inflation.

Agency MBS and Risk Assets

Agency MBS underperformed in June, with the Bloomberg US MBS Index returning negative 20 bps excess return, but overall 2026 performance remains solid, driven by many of the factors discussed in this publication in recent months. Performance across the coupon stack was mixed, with production coupons outperforming lower coupons on stronger TBA market dollar rolls.

Equity markets were mixed in June, with the S&P 500 generating a -1.0% total return, to end the strongest quarter since 2020. Performance of individual sectors continued to be highly bifurcated, with investors trying to decipher between winners and losers of the AI trade. As such, the increased capital expenditures of hyperscalers are being viewed with growing skepticism, while recipients of the money – chip manufacturers, energy infrastructure, and data center construction – continue to benefit. How long this rotation plays out remains to be seen. For now, equity and corporate bond markets are seeing increased capital demand, as the month included large capital raises from Alphabet, which raised $85 billion in an equity follow-on, and SpaceX, which successfully conducted the largest ever initial public offering on record. Investment grade corporate bonds saw $188 billion in supply, the busiest June on record.

Fed Update: The New Sheriff Kevin Warsh is in Town

The June FOMC meeting was less about the policy rate decision and more about regime change. As expected, the Committee unanimously held the Fed Funds Target Range at 3.50%-3.75%, but the bigger development came in Kevin Warsh’s first press conference as Fed Chair. He did not ease into the job but used the meeting to alter the Fed’s public signaling, cutting the policy statement to the shortest since 2002 and removing forward guidance entirely. Warsh said the statement was “a bit shorter, a bit simpler” and that forward guidance was “not well suited to the current policy conjuncture.” Despite the limited word count, the statement had enough room to signal a clear policy bias with the closing line stating that the “Committee will deliver price stability.”

The practical message was clear: a Warsh-led Fed is steadfast in its commitment to bringing inflation back to target and wants markets to react less to policymakers’ hints and more to incoming economic data. Said a different way, Chair Warsh appears to want the market to signal what the Fed should do rather than what it thinks the Fed intends to do. This represents a meaningful shift. Under recent Fed chairs, the Fed often tried to shape expectations by describing how it would respond if risks evolved. Warsh is moving in a different direction: fewer words, fewer commitments, and more signaling from markets towards the central bank.

The implications for volatility appear mixed. Streamlining the policy statement, eliminating forward guidance, and reducing the amount of Fed speak could lower volatility around Fed events, but shift them towards the data releases that guide monetary policy. The ultimate amount of total volatility delivered will be highly dependent on the clarity around the Fed’s reaction function. Absent forward guidance, markets will need a clear understanding as to how monetary policy will change under certain circumstances to avoid bouts of short-term rate volatility.

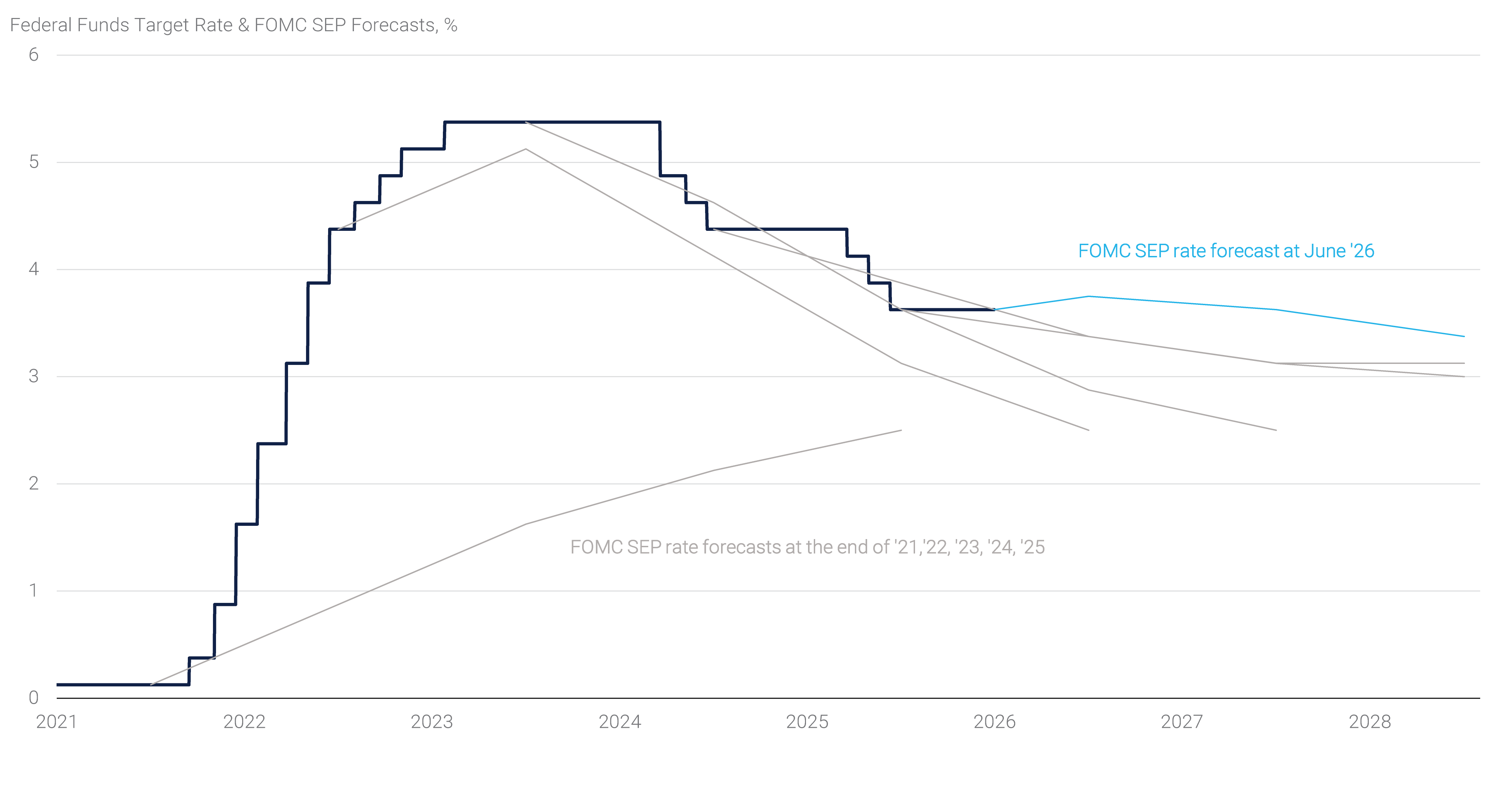

The Summary of Economic Projections (“SEP”) reinforced the meeting’s hawkish tone. The 2026 median funds-rate projection rose to 3.75% from 3.375% in March, with nine of eighteen FOMC members now penciling in at least one rate hike.(2) 2026 GDP growth was revised modestly downward, while unemployment projections improved slightly, and inflation forecasts moved meaningfully higher. Of note, Chair Warsh deliberately withheld his own submission which he rationalized by saying it was “not helpful in the conduct of policy.” In line with Warsh’s skepticism, market participants’ assessment of the rate forecasts contained in the SEP has grown more negative in recent months. And while a reform of Fed communications could ultimately lead to a better tool for the Fed to convey its reaction function, the median rate forecasts have been reasonably good indicators as to the direction of monetary policy in recent years. Although they were highly inaccurate at the end of 2021, more recent years have shown the actual rate and the Fed’s guidance to be relatively similar (see panel 4). Perhaps we are hanging on an antiquated communication tool, but we are conscientious that the new era will require some adjustments from markets.

Panel 4:

SEP Rate Forecasts Have Aligned With Policy Developments in Recent Years

In the spirit of reform, Chair Warsh announced the creation of five task forces to review Fed communications, the balance sheet and reserves framework, data sources and methodology, productivity and jobs in an era of transformation, and inflation frameworks. The communications review will include the SEP, dots, press conferences, meetings, transcripts, and minutes. The balance sheet review will examine the ample reserves regime and operating framework. The data review will look for (hopefully) more accurate and timely private sector or official sector sources. Finally, the inflation framework review will revisit the drivers of inflation and ideas for delivering price stability. Warsh said the task forces should begin work in the next couple of weeks, with initial framing in the fall and most, if not all, complete by year-end. The aggressive timeline will keep the task forces busy and lead to ample speculation about their outcome.

Altogether, there are two competing interpretations to the June FOMC meeting. The hawkish interpretation is straightforward: the statement centers price stability, drops two-sided risk language, removes forward guidance, and the SEP shifted meaningfully toward hikes. An alternative interpretation is that Warsh is trying to buy optionality. By launching reviews that conclude within the next year, he reduced the Fed’s near-term commitments while preserving room to lean on a productivity/AI narrative if inflation cools. For the time being, the Fed is now offering less explicit guidance, placing more emphasis on price stability, and reviewing nearly every major element of its policy apparatus. For markets, that means more weight on incoming data, more uncertainty around the reaction function, and a higher risk that the front end reprices abruptly when inflation or labor data surprise.