The longest government shutdown on record ended on November 12th, allowing statistical agencies to resume their work – much to our relief. But ending the shutdown did not translate into immediate economic data releases. Instead, we saw the release of some September data collected ahead of the government closure and the permanent loss of some October data. Meanwhile, we will have to wait to gauge economic activity data in the fourth quarter until the middle of December, when the Bureau of Labor Statistics (“BLS”) is scheduled to release the November non-farm payrolls (“NFP”) and Consumer Price Index (“CPI”) reports.

Economic Growth & Labor Market

Turning to the data received in November, the BLS released the September NFP report, with headline hiring figures better than expected, though the report ultimately did little to dispel the notion that the U.S. labor market is slowing. It is more of a moderation than a rapid deceleration in labor demand, but the unemployment rate rose for a fourth consecutive month to 4.44%, the highest level since October 2021. The increase in unemployment in August and September was primarily fueled by strong labor force participation, with more individuals entering the labor market than people able to find employment. While a reduction in labor demand appears to be the main driver of the labor market slowdown, a clear negative for job seekers, risks for inflation should be contained given more muted wage gains all else equal – a silver lining for the Federal Reserve’s (the “Fed”) conduct of monetary policy.(1)

This narrative generally jives with the stronger than expected hiring in September. Employers hired 119,000 workers, more than any economist surveyed by Bloomberg had expected, bringing the 3-month average to 62,000 from 18,000 in August (see panel 1). The healthy hiring was driven by sizeable increases in the leisure & hospitality and healthcare sectors, which added nearly nine out of ten jobs in the month. Of note, several Wall Street economists doubted the strength in the reported hiring in these sectors given overly beneficial seasonal adjustments, risking weaker hiring figures once numbers are revised in coming releases. While manufacturing industries saw job losses for the fifth consecutive month, construction hiring improved, at least temporarily ending a relatively notable weakness over the summer months.

Panel 1:

September Payrolls Surprised to the Upside

September retail sales disappointed expectations and sowed some doubt on the narrative of an unfazed consumer, particularly given the softer labor market and the continued weakening in consumer confidence readings. Retail sales rose 0.2% month-over-month (“mom”) in September following three very strong readings between June and August. The strong readings in earlier months buoyed Q3 2025 consumption (see panel 2), as the nominal control group spending(2) remained near 6.3% 3-month/3-month seasonally adjusted annualized rate (“SAAR”).

Panel 2:

Consumption Remained Supportive of Q3 GDP Growth

The September consumer data signals potential headwinds for consumption readings into Q4. For example, October vehicle sales fell to 15.3 million annualized vehicles, the weakest reading this year, perhaps suggesting some weakness in big-ticket item spending. Moreover, consumer confidence measures have generally continued to decline in recent months, with the November read on Conference Board consumer confidence declining to levels nearly 2 standard deviations below the 5-year average. Declining labor market prospects, continued price pressures – whether it be goods from tariffs or electricity prices – and the rise in healthcare insurance premiums and services appear to weigh on consumers. Finally, it is important to note that consumer experiences differ meaningfully across the income spectrum, as discussions around a “K-shaped” economy – one in which higher income levels do well, but lower income levels continue to struggle – have increased.

Inflation

After the release of the September CPI report in late October, the BLS released the October Producer Price Index (“PPI”) data last week that now paints a wholesome inflation picture for the upcoming Personal Consumption Expenditure (“PCE”) report release on December 5th. PCE prices excluding food and energy (“core PCE”) are expected to rise 0.25% mom based on the CPI and PPI data, suggesting that inflation will moderate only very marginally on a year-over-year (“yoy”) rate. Absent meaningful revisions to prior months, annualized core PCE in Q3 2025 should come in at 2.9% SAAR, higher than the 2.6% SAAR rate seen in Q2 2025. PPI details nonetheless offered some optimism by showing modest service sector inflation, boosting the argument that services prices are continuing to moderate even if goods prices are being impacted by tariffs. A similarly positive signal came from PPI trade services – the measure of corporate margins in the price index – which slowed to 1.5% yoy, the most benign reading in over a year.

Financial Markets

Over the past month, markets have contended with shifting Fed expectations, delayed economic data, and shifts in risk sentiment driven by renewed questions around AI capital expenditure. Volatility returned primarily in risk assets, reflecting the still uneasy balance between monetary policy uncertainty and changing growth narratives

Interest Rates and Monetary Policy

Treasury yields rallied through November, led by the front-end of the curve, with 2- to 5-year yields roughly 9 basis points (“bps”) lower and the 5s30s spread wider by 10 bps. The curve steepened as the front-end adjusted to increasingly dovish near-term policy debates, while intermediate and long-end yields stayed firmly anchored. Notably, the 10-year real rate ended the month unchanged, underscoring that markets still view the broader rate cycle, particularly terminal rate pricing, as largely stable.

The backdrop for these moves was complicated by the lingering effects of the U.S. government shutdown. With official data delayed, debate around the likelihood of another rate cut at the December meeting became unusually reactive, as each private-sector data point, survey release, and Fed remark carried outsized weight. At different points in November, market pricing swung sharply against a cut and then back in favor of one as investors tried to interpret a highly inconsistent stream of official Fed speeches.

The disagreement across policymakers has been both unusually public and unusually pointed. The hawkish contingent has argued that inflation remains too high, disinflationary progress has stalled, and interest rate cuts could increase pricing pressures. President Hammack (Cleveland, non-voter), who opposed October’s cut, said she would not support additional easing in December, warning that cutting too soon risks prolonging above-target inflation. President Logan (Dallas, non-voter) offered a similar view and President Goolsbee (Chicago, voter), typically more dovish, expressed discomfort with “front-loading too many cuts” given the economy’s resilience. By contrast, the dovish faction pointed to labor market softening and framed easing as prudent risk management. Governor Waller reiterated his preference for a December cut to hedge against rising employment risks, and President Williams (New York, voter) noted that policy is still “modestly restrictive,” suggesting there is room for further cuts in the “near term.”

This division was underscored by the October FOMC Minutes, which showed “several” participants favoring a cut and “many” preferring to hold rates steady through year end, language that again signaled a FOMC without a dominant consensus. Against this backdrop, market-implied odds of a December cut moved from roughly 25–35% early in the month to around 90–100% by month end, underscoring how quickly pricing moved amid scarce data and an unusually fractured communication background.

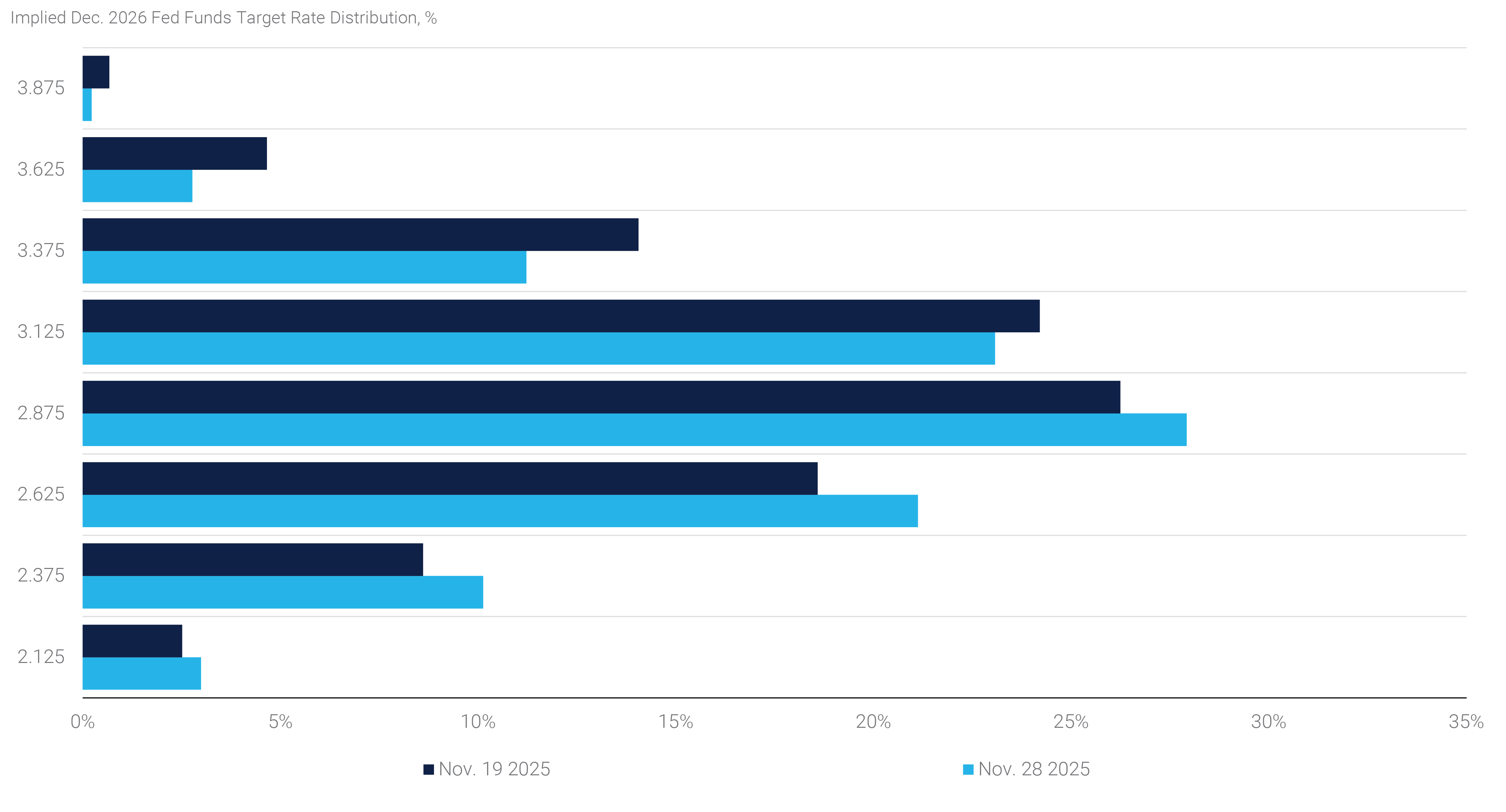

Yet despite all the attention on near-term cuts, markets remain firmly anchored in their medium- and long-term outlook. Overnight index swaps continue to price a policy trough near 3.0% by the end of next year. Even into the volatility around December 2025 cut probabilities, the terminal rate and estimated distributions around it moved only marginally in November (see panel 3). The stability in terminal rate pricing is especially notable given that the Fed will look markedly different next year under the leadership of a new Fed Chair. For now, markets seem comfortable with the idea that policy does not need to fall below the perceived neutral rate but are more focused on how quickly the Fed gets there.

Panel 3:

Medium- to Long-Term Rates Remain Well Anchored(3)

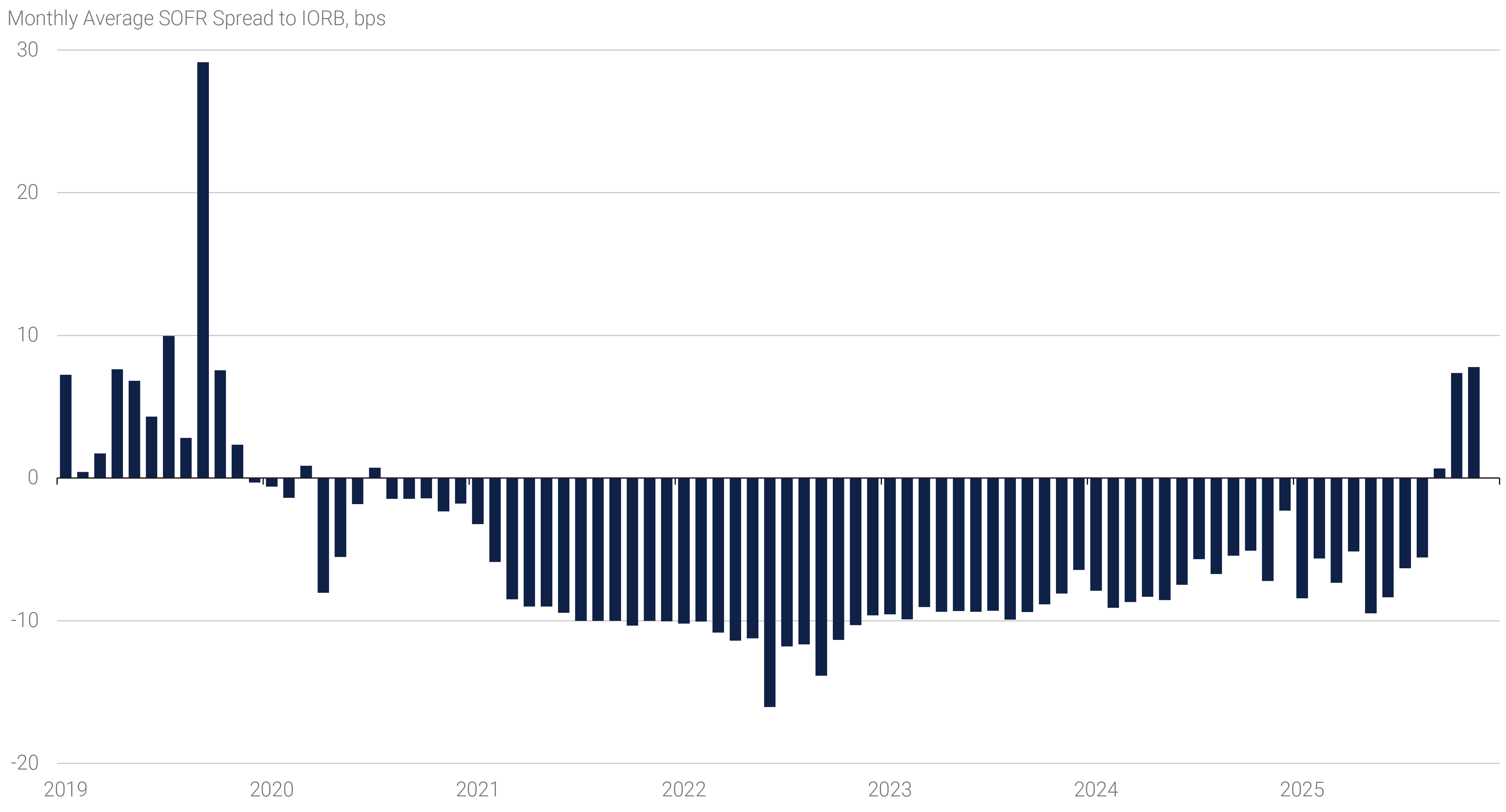

Short-term markets continued to see some volatility in November, though pressures eased somewhat relative to October. The Secured Overnight Financing Rate (“SOFR”) traded at an average spread of 7 bps relative to the Interest Rate of Reserve Balances (“IORB”) in November, essentially the same average spread as in October (see panel 4). The stability in the spread, an improvement compared to the widening over the summer months, was likely driven by lower Treasury bill issuance and a decline in the Treasury General Account, which reduced pressure on declining bank reserve balances at the margin.

Panel 4:

SOFR Spreads Highest Since 2019

Risk Assets

While the rates market has been shaped by the monetary policy debate, volatility in risk markets was fueled by a reassessment of the AI investment cycle. Equities saw a broad risk-off move, with major indices down as much as 5% at one point and the AI-themed stock complex experiencing declines of more than 10% from recent highs. A large portion of the move reversed late in the month, but the price volatility reflected a growing set of concerns: the sustainability of AI CapEx, rising customer-concentration risk, and questions around “circular financing” and the pace at which the ecosystem can absorb continued investment.

Leverage has become a more prominent part of that discussion as well. Credit markets are increasingly being used to fund AI-related CapEx, with issuance from AI-exposed companies rising meaningfully. As a result, credit spreads for investment-grade tech borrowers have widened relative to the broader market, a sign that investors are beginning to price in those risks more explicitly.

Positioning dynamics in equities also likely added to the downside pressure. There are clear signs of de-grossing into year end, likely amplified by retail flows, which helped extend the pullback into other speculative assets. Bitcoin, for example, dropped to a seven-month low, falling 17% in November, triggering large liquidations and wiping out more than $1 trillion in market value across the cryptocurrency complex.

Taken together, the move underscores how central the AI theme has become to macro sentiment. AI has driven much of this year’s growth optimism and provided a second-order boost to consumption through wealth effects as AI-heavy equities have propelled stocks higher. It now serves as the market’s key swing factor, capable of dictating direction even when the broader backdrop, including the prospect of a Fed easing cycle in a non-recessionary environment, would typically be supportive for equities.

Agency MBS

Despite the increase in equity volatility, interest rate volatility remained relatively contained over the month. Swaption-implied volatility in November averaged below October’s level, primarily driven by continued muted realized interest rate moves. The limited economic data releases, combined with the perceived stable medium-term outlook for monetary policy, likely contributed to the low volatility. In this environment, Agency MBS spreads remained generally well supported, with the Bloomberg MBS Index posting a modestly negative excess return of -0.05% for the month. Early in the month, investors had to digest a very fast prepayment speed report for October, when borrowers signaled a high propensity to refinance their mortgages in just modestly lower interest rates. The reactive refinancing activity in standard mortgage pools appears driven by high loan sizes and good consumer credit scores, both of which make it easier to refinance existing mortgage loans. In addition, mortgage originators have ample capacity as demonstrated by one of them running an incentive program to increase refinancing. We believe that that program, which ended in mid-September, helped drive refinancing activity meaningfully.